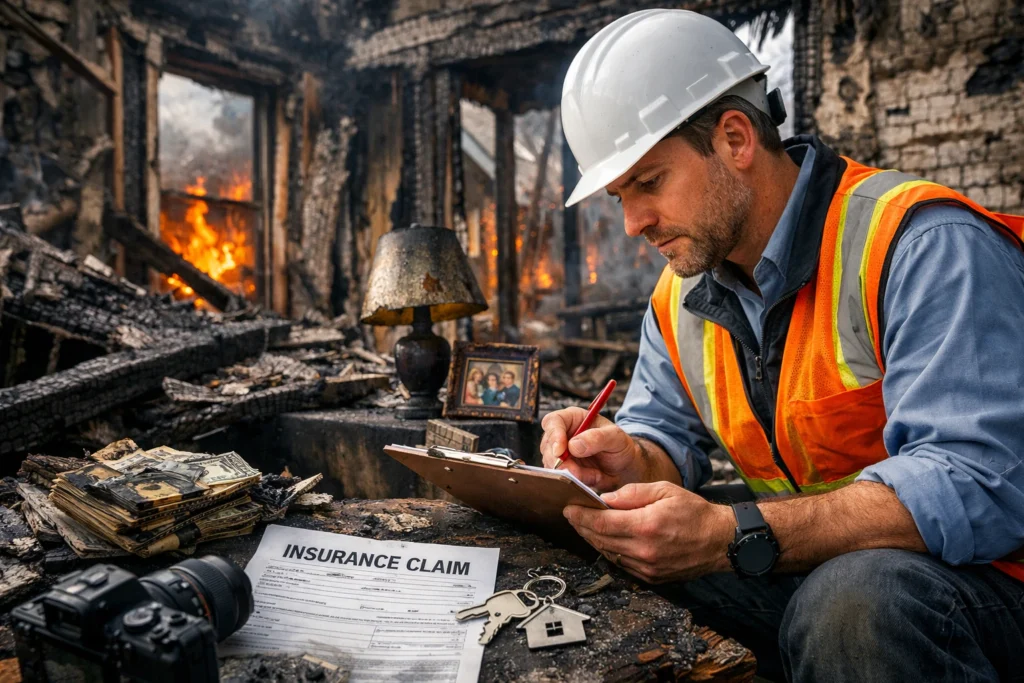

A house fire changes everything in a matter of minutes. One moment you’re living your routine, and the next, you’re dealing with smoke, damage, loss, and a flood of decisions. This is exactly when a fire insurance adjuster enters your life and what they do next can directly impact how much money you recover.

I’ve seen it happen too often. Homeowners assume the insurance process will be straightforward. It rarely is. The difference between a stressful, underpaid claim and a fair, fully compensated one often comes down to understanding how the system works and who is actually on your side. If you’re in Sugar Land or nearby areas, this matters even more. Local building costs, contractor availability, and regional policies all influence your claim. Let’s break it down in a way that actually helps you make smarter decisions.

What Is a Fire Insurance Adjuster?

A fire insurance adjuster is the person responsible for evaluating your fire damage claim and determining how much your insurance company should pay. Sounds simple. It isn’t.

There are actually three types of adjusters you need to understand:

- Insurance Company Adjuster – Works for your insurance provider

- Independent Adjuster – Contracted by the insurance company

- Public Adjuster – Works for you, the homeowner

That distinction? It’s everything.

An insurance adjuster is focused on protecting the company’s bottom line. A public adjuster focuses on maximizing your payout. Same process. Completely different goals.

How a Fire Insurance Adjuster Evaluates Your Claim

When a fire insurance adjuster arrives, they’re not just taking a quick look around. They’re building a case one that determines your financial recovery.

Here’s how that process typically unfolds:

Step-by-Step Breakdown

- Initial Inspection

They walk through the property, documenting visible damage. - Damage Documentation

Photos, notes, and measurements are taken. - Estimate Creation

Repair and replacement costs are calculated. - Policy Review

Coverage limits and exclusions are applied. - Settlement Offer

You receive a number. Often lower than expected.

What They Look For

- Structural damage (walls, roof, foundation)

- Smoke and soot contamination

- Water damage from firefighting efforts

- Personal belongings and inventory loss

Here’s the problem: what they don’t include can cost you thousands.

The Hidden Challenges Homeowners Face During Fire Claims

Fire claims are complex. Emotionally draining. And full of traps.

Let’s be real this isn’t something most people are prepared for.

Common Issues You’ll Face

- Undervalued damage – Hidden damage is often missed

- Incomplete inventories – Many items never get claimed

- Policy confusion – Terms are easy to misunderstand

- Delays – Weeks turn into months

- Low initial offers – Insurance companies test your response

When you’re stressed, overwhelmed, and trying to rebuild your life, it’s easy to accept what’s in front of you. That’s exactly what insurance companies count on.

Fire Insurance Adjuster vs Public Adjuster What’s the Difference?

This is where things get interesting.

| Feature | Insurance Adjuster | Public Adjuster |

| Who they work for | Insurance company | You (policyholder) |

| Goal | Minimize payout | Maximize payout |

| Negotiation | Limited | Aggressive |

| Claim control | Insurance-led | Homeowner-led |

Let’s simplify it.

- A fire insurance adjuster from the insurance company evaluates your claim.

- A public adjuster challenges and negotiates that evaluation.

One protects the company. The other protects you.

Why Hiring a Public Fire Insurance Adjuster Can Increase Your Settlement

If there’s one move that changes the entire game, it’s this. Hiring a public adjuster shifts the balance of power.

Here’s Why It Works

- Detailed Documentation

Every item, every damage point, every cost is accounted for. - Accurate Valuation

Not just what something is worth but what it costs to replace today. - Negotiation Expertise

They speak the same language as insurance companies. - Time Savings

You focus on rebuilding your life. They handle the claim.

In many cases, homeowners who work with a public adjuster receive significantly higher settlements. Not slightly higher. Significantly.

The Fire Damage Claim Process Step-by-Step Guide

After a fire, everything feels chaotic. But the process itself follows a structure.

What Happens Next

- Ensure Safety and Secure Property

- Notify Your Insurance Company

- Meet the Fire Insurance Adjuster

- Damage Assessment Begins

- Receive Initial Settlement Offer

- Negotiation or Acceptance

Simple on paper. Complicated in reality. Each step has opportunities and risks.

Common Mistakes to Avoid When Dealing with a Fire Insurance Adjuster

Mistakes are expensive. Some cost thousands. Others cost your entire claim potential.

Avoid These at All Costs

- Accepting the first offer too quickly

- Failing to document everything thoroughly

- Throwing away damaged items prematurely

- Misinterpreting your policy coverage

- Waiting too long to seek professional help

One wrong move early can limit your options later.

How to Prepare Before the Adjuster Arrives

Preparation changes everything. If you’re ready, you control the narrative. If you’re not, you react.

Do This Immediately

- Take photos and videos of all damage

- Create a room-by-room inventory list

- Gather receipts, warranties, and proof of ownership

- Prevent further damage (board up, tarp, etc.)

- Keep a log of all communication

This isn’t just busywork. It’s leverage.

What Does a Fire Insurance Adjuster Look for in Damage?

A fire insurance adjuster isn’t just checking what’s burned. They’re evaluating the entire property ecosystem.

Key Areas of Focus

- Structural Integrity – Can the building be repaired or rebuilt?

- Electrical Systems – Fire often compromises wiring

- HVAC Systems – Smoke contamination spreads through vents

- Hidden Damage – Behind walls, under floors

- Water Damage – From extinguishing efforts

Even the way heat travels through materials can affect the outcome of your claim. This phenomenon is sometimes influenced by thermoelasticity, which explains how materials expand and react under extreme heat something adjusters indirectly account for when assessing structural integrity. Missing even one of these can lead to serious underpayment.

How Long Does a Fire Insurance Claim Take?

This is the question everyone asks. The answer? It depends.

Typical Timeline

- Small claims: 2–6 weeks

- Moderate damage: 1–3 months

- Major losses: 3–12+ months

What Slows Things Down

- Incomplete documentation

- Disputes over damage value

- Insurance company delays

- Contractor estimate conflicts

A public adjuster often speeds this up not by rushing, but by eliminating back-and-forth.

Understanding Your Insurance Policy After a Fire

Your policy is the rulebook. But most people never read it until it’s too late.

Key Terms You Need to Know

- Replacement Cost – Cost to replace items at today’s prices

- Actual Cash Value (ACV) – Depreciated value

- Coverage Limits – Maximum payout

- Deductibles – Your out-of-pocket cost

- Additional Living Expenses (ALE) – Temporary housing and costs

Understanding these terms can mean the difference between partial recovery and full recovery.

When Should You Call a Public Adjuster in Sugar Land?

Timing matters. Waiting too long can limit your options.

Call a Public Adjuster If:

- The fire just happened

- Your claim is delayed

- The offer feels too low

- Your claim is denied or underpaid

Early involvement often leads to stronger outcomes.

Real-Life Example Fire Claim Settlement Comparison

Let’s put this into perspective.

Scenario Comparison

| Situation | Without Public Adjuster | With Public Adjuster |

| Initial offer | $85,000 | $85,000 |

| Final settlement | $92,000 | $145,000 |

| Time to resolve | 6 months | 3–4 months |

That gap? It’s not unusual.

It’s the result of better documentation, stronger negotiation, and knowing how to push back.

How Sugar Land Public Adjuster Helps You Win Your Claim

This is where local expertise makes a difference. Sugar Land isn’t just any market. Construction costs, local codes, and contractor pricing all influence your claim.

What You Get

- Local knowledge of rebuilding costs

- Hands-on claim management

- Thorough documentation and valuation

- Aggressive negotiation with insurers

- Less stress during an already difficult time

You don’t just get help. You get representation.

Final Thoughts Take Control of Your Fire Insurance Claim

A fire takes enough from you already. Your insurance claim shouldn’t take more. The truth is simple. A fire insurance adjuster plays a critical role in determining your financial recovery. But not all adjusters are on your side. Understanding that difference is the first step toward protecting yourself.

Be proactive. Document everything. Ask questions. And if something doesn’t feel right, trust that instinct. Because in the end, this isn’t just about a claim. It’s about rebuilding your life and getting every dollar you deserve.

FAQs

A fire insurance adjuster evaluates property damage, reviews your policy, and determines how much your insurance company should pay for your claim.

You can rely on their process, but remember they work for the insurer, so their goal is often to minimize payouts.

A fire insurance adjuster works for the insurance company, while a public adjuster represents you and negotiates for a higher settlement.

It’s best to hire one as early as possible, ideally before or during the initial claim evaluation process.

Most public adjusters work on a contingency fee, meaning they take a percentage of the final settlement rather than charging upfront.

Yes, but without experience, you may overlook damages or undervalue your claim, which can reduce your payout.

Avoid making guesses about damage or admitting fault stick to facts and documented evidence.

Document everything thoroughly, understand your policy, and consider hiring a public adjuster to advocate on your behalf.

You can dispute the estimate, request a re-evaluation, or bring in a public adjuster to negotiate a better outcome.

It can take anywhere from a few weeks to several months depending on the complexity of the damage and the negotiation process.